About this Issue

High-denomination currency joins together two seemingly unrelated subjects: macroeconomics and crime. Criminals love high-denomination paper money because it’s valuable and largely untraceable. Payments in cash can also be made off the books; indeed, it’s easier not to record such transactions than to record them, which enables tax evasion.

But high-denomination paper money is also where a great deal of the total cash of any economy will tend to reside. Regulations on this type of money can have macroeconomic effects that may harm lawful consumers and businesses. There’s a trade off, then, between law enforcement and crime deterrence on the one hand, and monetary policy on the other.

Joining us this month are four economists who have examined this problem. Finance journalist J.P. Koning writes the lead essay, in which he argues for large notes that gradually depreciate relative to small notes or bank deposits; this would discourage people from holding them for too long. Doing so would also capture the value now being lost to tax evasion, and in effect it would tax criminal transactions. Responding to him will be James McAndrews, formerly of the Federal Reserve Bank of New York; Professor Joshua R. Hendrickson of Mississippi State University; and Cato adjunct and Professor William J. Luther of Kenyon College.

Lead Essay

The Big Problems with Big Denomination Bills

When a shortage of coin prevented him from paying his troops, Jacques de Meulles—the administrator of the French colony of New France—resorted to using playing cards. Thus in 1685 the Western world’s first paper money was created. De Meulles only intended his playing card money to be a temporary back-up to specie. When coin arrived in the next boat from France, he promptly redeemed the entire issue. But over the years, Quebec’s administrators would resort to ever larger amounts of playing card money to meet citizens’ demand for cash.

Little did de Meulles know that hundreds of years later, his paper-money invention would be serving as a different sort of back-up system. Banks and credit card networks are processing a growing proportion of society’s transactions. These financial institutions are privy to an ever-expanding slice of our lives. Do we trust banks to do a good job guarding this information? Perhaps they may accidentally allow hackers access to it, or they may be forced to give the government a quick glance at what we’ve purchased over the last month. Cash, on the other hand, leaves no trace of what we’ve bought or sold. No other payments medium allows us to be 100% sure that our personal information can never be seen by someone else.

Not only does cash protect our data, it provides us with irrevocable access to the payments system. Electronic payments systems are run by central authorities with the power to censor users. In 2010, for instance, Bank of America, MasterCard and VISA embargoed Wikileaks, effectively cutting it off from receiving payments. Or consider the case of UK-based NGO Interpal. After it was accused of terrorist financing by the U.S. government and sued by families of the victims of bombers, Interpal accounts at a succession of UK banks were shut, despite the fact that the Charity Commission for England and Wales—a government department that regulates registered charities—cleared the NGO three separate times of the accusations.

More recently, U.S. banks have been unwilling to open accounts for marijuana firms. Even though many states have legalized marijuana sales, federal law continues to treat marijuana as a drug on par with heroin. Like Wikileaks and Interpal, the marijuana industry has been able to fall back on cash to survive. Cash is decentralized. Banknotes move from hand to hand rather than requiring permission from a central processor. The advantage of this is that there is no third party that can insert themselves between two willing transactors and prevent them from consummating a deal. In a sense, cash is society’s payments-system-of-last-resort.

U.S. dollars are not only used by Americans but are also a popular means for foreigners to protect themselves from inflation of the domestic currency. The most marked example of this is Zimbabwe. In late 2008, with inflation hitting 79,600,000,000% per month, Zimbabweans spontaneously threw their Zimbabwe dollars into the trash and started buying and selling things with U.S. dollars. The economy’s galloping price level suddenly came to a halt.

U.S. banknotes are also popular in countries with corrupt banking systems. In early 2016, lineups began to grow outside of Zimbabwean banks as locals tried to withdraw banknotes. Lacking enough reserves to meet these requests—a large chunk of the banking system’s resources had been confiscated by then-leader Robert Mugabe—the banks began to set strict daily withdrawal maximum of around $30. By late 2016, all deposits would be unofficially redenominated. Sadly, this meant that any Zimbabwean who had funds stuck in the domestic banking system had had a significant chunk of their wealth stripped from them. Those who held their wealth in U.S. dollar form preserved their purchasing power.

Zimbabwe’s example illustrates how the U.S. dollar serves as the world’s backup monetary system. When people’s wealth is arbitrarily threatened by those in power, U.S. banknotes serve as an escape hatch.

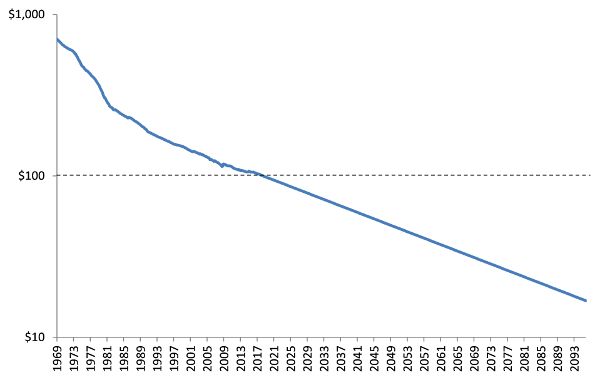

The ability of U.S. paper money to provide censorship resistance, data protection, and to act as the globe’s back-up monetary system has steadily declined over the years. Low-denomination banknotes like the $1 and $5 are excellent for providing small amounts of the above services. But to enjoy larger flows of these services, $1s and $5s are too bulky—higher denomination must be brought into service. Here’s the catch. Inflation has been eating away at the purchasing power of the U.S.’s highest denomination banknote, the $100 bill. Back in 1969, one $100 could buy 700 dollars’ worth of 2018 goods. Put differently, in 2018 it takes seven bills to do the work of just one.

Figure: Real value of the $100 bill, log scale

At inflation rates of 2% or so, by 2047 the $100 bill will buy as much as a $50 bill does today. By 2090, it will be capable of purchasing the same amount as today’s $20, and a hundred years from now its purchasing power will be the same as a modern $10 bill. That’s right—in 2118 the highest denomination note would be good for just two big Macs.

Introducing a new supernote, say a $500 or $1000, would stabilize this trend. With a new highest denomination banknote, U.S. cash would be able to provide society with the same convenient data protection that it did in the past. And by reducing the monetary workload that cash users must endure, a supernote would continue the U.S. dollar’s long tradition of providing both Americans and foreigners with a low-cost alternative to those who have been censored or face the threat of wealth confiscation.

If there are good arguments in favor of a new supernote, there are also good arguments against it. In his 2016 book The Curse of Cash, Kenneth Rogoff ignited a fiery debate by calling for an end to high-denomination banknotes. Rogoff’s refrain has been taken up by others, notably Peter Sands, a former bank executive, and economist Larry Summers.

There were some 12.5 billion $100 bills in existence at the end of 2017, or thirty-eight $100 bills per American. This simply doesn’t reflect the personal experience of most citizens. Indeed, 2012 survey data shows that consumers generally report holding just $56 per person. This number is bloated by the large amount of U.S. currency circulating overseas. But even in Canada, which does not issue an internationally accepted currency, there are thirteen $100 Canadian bills outstanding per citizen, far in excess of the amounts that most Canadian keep in their wallets or their cookie jars.

Proceeding from this observation, Rogoff reasons that high denomination banknotes are primarily used by criminals and tax evaders. By removing these denominations and forcing criminals to rely on smaller denominations like the $5, Rogoff contends that crime would become a less profitable endeavor. As for tax evaders, they would be pushed into the formal economy. This, he contends, would be beneficial for government finances. With less tax evasion, government revenues would rise.

The current U.S. policy of allowing the purchasing power of the $100 bill to wilt rather than introducing new higher denomination notes is a drawn-out version of what Rogoff advocates. Instead of cutting the highest denomination note’s purchasing power in one fell swoop, this same effect is occurring slowly via inflation. Rogoff would oppose the introduction of a new supernote for the same reason that he calls for a ban on the $100. A new supernote, say a $1000 bill, would be a boon to tax evaders and organized crime. According to Peter Sands, $10 million one-hundred dollar bills weighs 10 kilograms, an amount that a drug dealer could fit into seven briefcases. Using $1000 notes, that amount would fit into one briefcase with plenty of room to spare. Avoiding taxes by paying a contractor in supernotes would be easier too.

A number of arguments have been mounted against Rogoff’s proposal. William J. Luther, Larry White, and Jeffrey Rogers Hummel have all pointed out that much of the goods and services that are exchanged in the informal cash-using economy occur between consenting participants and do no harm to third-parties. This includes goods and services like prostitution and marijuana. Just because high-denomination banknotes help facilitate these activities does not necessarily mean that society would be made better off if these notes, and the trade they facilitate, were not provided.

James McAndrews contends that if high-denomination banknotes were to be removed, organized crime networks might launch an effort to create an underground payments system of their own. Without recourse to the courts, the mob would use force to manage this system. So by ceding the anonymous high-value payments business to criminal enterprises, the central bank would actually be responsible for increasing the amount of violent crime in society rather than reducing it. McAndrews’s criticism focuses on a “one fell swoop” scenario in which the $100 and $50 are removed. But assuming the United States refuses to issue a new super note, and inflation continues to eat away at the value of the $100, the scenario he criticizes will emerge with time.

These objections somewhat reduce the appeal of crime suppression as a motive for quashing high-denomination banknotes. That leaves tax evasion. Tax evasion creates equity problems. For instance, if contract workers can evade their taxes by accepting banknotes but an otherwise equivalent salaried employee cannot, the salaried employee bears the burden of making up for the tax gap caused by the contract employee. This hardly seems fair. A supernote would only increase this inequity. Cash-induced tax evasion can also lead to economic distortions. A project with high returns might lose funding to a low-return project only because the latter can avoid being taxed thanks to greater reliance on cash sales.

If there ever was a tough balancing act, this may be it. Providing civil society with consistent levels of censorship resistance, freedom from data snooping, and a fully functioning back-up monetary system are all important. But these services will inevitably be abused.

But there may be a way to provide a new highest-denomination note while also developing a mechanism for coping with some of the negative externalities created by that note. The idea is to tax the new note.

This may come as a surprise, but banknotes are already taxed, albeit not explicitly. Anyone who holds a $1 bill is forfeiting around two cents per year in interest. This tax could be removed if the Federal Reserve paid interest on banknotes (say in the form of a serial number lottery), or if it set nominal rates at zero so that owners of notes needn’t lose out on any interest. Although notes are taxed, this hasn’t hurt their popularity. In the U.S., the quantity of banknotes in circulation continues to grow at 6.8% year, in line with the 35-year average growth rate of banknotes and well above nominal GDP growth.

The current tax on banknotes is a flat tax. Owners of large denomination $100 notes pay the same tax rate as owners of small denomination $1s and $5s. This doesn’t seem fair. If illicit usage of notes becomes more prevalent as the denomination of notes rises, it makes sense for the tax rate on high-denomination notes to be higher than that on low-denomination notes. Under this tax regime, those engaged in the sorts of illicit activities facilitated by high denomination notes will also bear the costs of the externalities they create.

It is relatively easy to set a higher tax on supernotes than on other denominations. Say that an extra 5% surcharge is deemed adequate to offset the externality caused by supernote users. On the first day that the supernote is issued, the Federal Reserve sets the value of the supernote at $1000. It does so by promising to redeem all supernotes with $1000 worth of other notes and/or electronic reserves. On the second day, it reduces its redemption rate by fifteen cents, to $999.85, and the day after to $999.70. By the end of the first year, the supernote would be worth around $950, fifty dollars less than its initial value.

The effect this has is that anyone who had held one thousand $1 bills over that period would have been taxed at the regular rate of about 2% per year, or $20 in real value. But anyone who had held the supernote would be taxed not only the $20 but an additional $50. This $50 would be used by the government to plug the hole caused by supernote-facilitated tax evasion and the extra work required on the part of law enforcement officials.

To get the Federal Reserve’s exchange rate for the supernote on any particular day, people could simply check the Fed’s website. To make things less complicated, the Federal Reserve could print the new notes without a denomination, just like how medieval coins were issued. The new note would be nicknamed the (Susan B.) Anthony, or the Lincoln, or whomever, depending on whose face was printed on it.

The tension between the important services provided by the highest denomination note and the potential for those properties to be abused make this issue especially complex. The monetary authorities have currently settled on a “Rogoff-lite” policy of slowly reducing the ease of accessing the vital services provided by U.S. cash. As time passes and inflation eats away at the $100, the risks of reducing the convenience of the array of U.S. banknotes will grow. A supernote, one that bears an extra tax relative to other banknotes, is one option for settling some of these tensions. It ensures that U.S. paper money continues to provide the same services as before while also trying to capture a toll from abusers.

Response Essays

A More Modest Proposal

Does the United States need to provide a high-denomination “supernote” of $500 or $1,000? In a stimulating essay, J.P. Koning suggests that such a note, combined with a means to tax it, could improve economic outcomes. His proposal derives from his recognition that currency provides a flow of services by facilitating transactions that are valuable to society. Currency has a dark side, however, in its use as an untraceable way of evading taxes and prohibitions on criminal activities. Currency’s services are threatened by the steady onslaught of inflation that has eroded its value over time, effectively limiting the range of transactions, both good and bad, that it can best facilitate. In terms of its buying power, the $100 bill just ain’t what it used to be. Koning’s proposal to introduce taxed supernotes is a way both to arrest the erosion of currency’s services and to discourage excessive use of high-denomination notes.

Koning’s proposal has two parts. Rather than simply issue a new high-denomination note, the new note would be taxed. Let’s consider these two separate aspects of the proposal in turn: the introduction of the supernote and the taxation of high-denomination notes.

Koning provides a sound characterization of the services provided by currency in its transactions role: censorship resistance, data protection, and the ability to act as a backup for the global monetary system. These attributes allow currency to provide unique transactions services. If currency weren’t available, many transactions simply would be foregone—so providing currency is an important public service. With positive but low inflation in most of the advanced nations in recent decades, the real value of fixed nominal denominations has declined significantly, though gradually. The gradual reduction in real values, combined with the introduction of convenient credit and debit cards, allowed people to adjust to the lower value of particular denominations by using alternate means of payment.

Koning is nonetheless rightly concerned that the reduction in real value of current denominations may cause society to lose some of the benefits of currency. Again, if the largest U.S. note 50 years ago was seven times the value of today’s largest note in real terms, it is worth asking what we have lost or gained in the transition. To stop the inflation-induced reduction of services provided by currency, Koning suggests a bold remedy: introduce a high-denomination note. This could be something like the $100 bill of 50 years ago, equal in today’s dollars to a $500 or $1,000 note.

The suggestion that the U.S. introduce a $500 or $1,000 note draws our attention to an important question: what is the best system of denominations for U.S. currency? Relative to fifty years ago we have had the unprecedented development of credit and debit cards, the introduction of the internet and online banking, and more recently, innovations of convenient person-to-person mobile payments. All of these changes have certainly assisted people in substituting away from currency as its denominations have diminished in real value. Over the same period, however, the demand for currency and its services has risen as inflation and economic growth have tended to increase nominal transaction sizes, income inequality has widened, and the absolute number of people without bank accounts has grown. It is plausible that a denomination system with some higher denominations would provide a better match to today’s transactional demand for currency, although that proposition is far from certain.

The intention of a tax on high-denomination currency would be to reduce illicit and illegal activities. High-denomination notes are especially useful in currency’s illicit and illegal uses—a $100 note is a hundred times more valuable than a $1 note but is equally cheap to carry and store. This trait, along with the untraceability of currency, makes high-denomination notes more convenient for large transactions and for storing ill-gotten gains. A tax on high-denomination notes would tend to diminish their quantity demanded. People engaged in transactions that would otherwise use high-denominations notes would either forego the transaction, or find some less convenient workaround, using another means of payment, such as cybercurrency.

All currency is subject to an implicit tax, since currency earns no interest and suffers a reduction in value from inflation. Koning proposes adding an additional tax on supernotes by issuing them at par and redeeming them for lesser amounts. For example, it would cost $1,000 to obtain a $1,000 note, but whenever in the future the note would enter the banking system, it be redeemed for something less than $1,000, depending how long it has circulated.

Taxing high-denomination notes has significant drawbacks. First, the specific form of taxation that Koning suggests, namely a lower redemption value over time, assessed whenever a note enters the banking system, relies on market participants to correctly gauge and enforce the current value of the note. That calculation is a difficult one in the decentralized circumstances in which cash transactions occur. It is also unlikely that the tax would be widely enforced as currency changes hands in decentralized transactions, especially in circumstances in which there is coercive power on one side of the deal, something that is common in illegal activity. Furthermore, note-holders could simply avoid depositing the notes in the banking system for years and years, thereby effectively avoiding the tax.

It is important to state that a tax on high-denomination notes is not a Pigouvian tax, one that taxes a noxious activity, such as imposing an excise tax on the output of a factory that creates pollution. Instead, it is a tax on an input to activities, only some of which may be noxious. That is akin to taxing the labor that could be used in the polluting factory or in a nearby nonpolluting garden. Taxing inputs that can be used for good or bad purposes will regrettably impose taxes on some good uses of the input, in this case high-denomination notes.

The combination of a high-denomination supernote and a way to tax that note is an intriguing proposal, as it attempts to reckon with both the falling real value of currency and the service that high-denomination notes provide to some tax-evasion and criminal activities. Whether a supernote is warranted is difficult to determine, but to introduce a $500 or $1,000 note would represent a relatively dramatic change in the current denomination structure and would require more convincing evidence than we have at present. Taxing different denominations differently would tax beneficial uses of currency along with the unsavory ones, and the form of the proposed tax makes it unlikely to be widely enforced in practice. Perhaps an alternative proposal with the same goals as Koning’s would be to introduce a $200 denomination note, and to increase expenditures devoted to detecting violations of our nation’s laws and on enforcement of those laws, especially those related to money-laundering, tax evasion, and terrorist funding.

Do High-Denomination Notes Create Externalities?

In J.P. Koning’s lead essay he outlines the costs and benefits of large denomination currency and proposes the introduction of a high-value “supernote” that would be taxed to deal with the externalities imposed by high denomination users. Koning’s proposal is similar to the optimal policy suggested in my own work with my colleague, Jaevin Park. It should therefore come as no surprise that I would support his policy proposal on the condition that we accept the premise that there are externalities imposed by the use of currency.

However, I am not completely convinced by that premise. As such, I would like to organize my response around three points. First, I will push back on the idea that the use of currency creates an externality in the traditional sense that we use the term. Second, I will argue that the elimination of high denomination notes would do little to reduce illegal transactions. And finally, I will argue that even if we accept the premise that currency creates an externality, the optimal policy would not be to eliminate high denomination notes, but rather to enact the sort of policy that Koning proposes.

A common argument made by those advocating the elimination of high denomination notes (or currency, entirely) is that currency is used in illegal trade and therefore creates an externality that needs to be corrected by public policy. This argument is predicated on a different view of externalities than is typically found in the literature. For example, pollution is a textbook example of an externality. A firm that generates pollution as a byproduct of production does not bear the full cost of the pollution. Since the pollution can affect air quality and/or the health and production of others in society, the firm is creating an external cost above and beyond the cost of its own production. It is important to note that the cost to society is not the mere annoyance of seeing clouds of smoke or murky water, but rather the health and productivity consequences of pollution. It is unclear whether the sort of illegal activity that is facilitated by currency fits the same model as something like pollution.

An externality is not simply any action that imposes a cost on others. If a new restaurant opens up across the street from an existing restaurant, the incumbent might incur a cost in the form of lower profits. However, this is not an externality that requires a public policy solution. Thus even if an activity is made illegal precisely because a vast majority of the population considers the transaction to be morally abhorrent, this does not necessarily imply that there is an externality. Pearl clutching, like foregone profits, are an external cost. Nonetheless we do not compensate firms for foregone profits, and therefore it is unclear whether mere distaste requires any sort of compensation. To the extent to which illegal trade is said to generate an externality, the external costs of such transactions are likely overstated.

Even if we accept the idea that the sort of illegal trade facilitated by currency generates an externality, there is no guarantee that eliminating currency (or the large denomination variety used in large-scale illegal transactions) would eliminate such trade. With respect to illegal trade, currency is a means to an end. Eliminating the means hardly guarantees an elimination of the end. Instead, those who are already engaged in illegal transactions are likely to look for substitutes. The recent emergence of cryptocurrency would likely get a boost from the elimination of large denomination conventional currency. Furthermore, those engaged in illegal activity might be inclined to create their own media of exchange or payment system.

All of this is not to mention the fact that currency (even large denomination currency) is used by many people for legal transactions. Eliminating large denomination currency therefore imposes a cost on the law-abiding members of society. This subtracts from any perceived net benefit of eliminating illegal trade. Overall, this suggests the net benefits of eliminating large denomination currency are likely exaggerated as well.

This brings me to my final point. Suppose that we simply take as given that illegal trade reduces social welfare, and that large denomination currency facilitates that type of trade. What should be done? What is the optimal policy? A typical Pigouvian response to this sort of problem is to levy a tax on the activity that creates an external cost. The proceeds of the tax can then be transferred to the harmed group. The problem with this type of policy solution is that illegal trade tends to be hidden and unreported and is therefore difficult, if not impossible, to tax.

The fact that large denomination currency has desirable properties for engaging in illegal activity, however, allows for a possible solution. As my colleague Jaevin Park and I show in our paper “Breaking the Curse of Cash,” the optimal policy in this sort of environment is to have two types of currency with a flexible exchange rate between the two currencies. Policymakers can then vary the rates of return (or the rates of depreciation) on each currency to induce legal traders to hold one type of currency and illegal traders to hold the other type. The seigniorage earned from depreciating the currency used by illegal traders can then be used to finance a transfer to legal traders. By introducing a separate type of currency, policymakers are able to engineer a Pigouvian policy.

The policy suggested by J.P. Koning in his original post is precisely the sort of policy consistent with our model. He argues that the United States should create a supernote and institute a surcharge (tax) on this supernote such that it depreciates faster than smaller denominations. If the tax is set optimally, this scheme would effectively replicate the result from our paper. To the extent to which we want to reduce illegal activity facilitated by cash, this is an appropriate policy to do so.

Subsidize the Supernotes. And the Others Too.

In a provocative essay, J.P. Koning argues that the U.S. government should issue supernotes—in denominations of $500 and $1,000. His proposal stands in sharp contrast to those offered by the demonetization crowd, which would see existing large denomination notes scrapped entirely and small denomination notes replaced with bulky coins. Koning claims supernotes would preserve the “ability of U.S. paper money to provide censorship resistance, data protection, and to act as the globe’s back-up monetary system” as inflation continues to erode the real value of the dollar. He also attempts to appease demonetizers by subjecting these supernotes to a supertax, which might be levied at the point of redemption.

I completely agree with Koning in the abstract. There are good reasons to issue supernotes. And, if these supernotes are primarily used to break just laws and to evade optimal taxes, it makes sense to tax them at a higher rate than lower denomination notes. When it comes to the real world, however, Koning and I part ways. Although I agree that the U.S. government should issue supernotes, I believe taxing these notes at a higher rate is unjustified. Supernotes (along with all other denominations) should be subsidized, in the form of a steady and gradual deflationary policy, under which nominal prices would tend slowly to decline over time.

For starters, it is anything but clear that large denomination notes are primarily used by criminals and tax cheats. Let’s start with the high-end estimate offered by Ken Rogoff in his 2016 book, The Curse of Cash (Princeton University Press), which I have described at length elsewhere. Rogoff claims 39 percent of all U.S. notes in circulation are employed by criminals and tax cheats in the domestic economy. The Federal Reserve reports $1,571.1 billion worth of U.S. notes in circulation in 2017, of which $1,251.7 billion was in $100 bills. If we assume that criminals and tax cheats only use $100s, Rogoff’s high-end estimate implies that roughly 49 percent of $100s in circulation facilitate illegal transactions in the domestic economy.

If, instead, we were to take the larger estimates Rogoff reports for currency held abroad (70 percent) and what is admitted to being held by domestic consumers in surveys (10 percent), the estimated shares of all cash and of 100s employed by criminals and tax cheats in the domestic economy fall to just 14 and 18 percent, respectively. And, if one suspects that some law-abiding cash users under-report their cash holdings in surveys—perhaps to keep those balances secure or because they are especially concerned with financial privacy—or that criminals and tax cheats use lower denomination notes as well, the estimates fall further still.

Even if one takes the high-end estimate offered by Rogoff at face value, it is important to realize that some crimes are welfare-improving. We do not live in a world where only just laws make it onto the books. Some laws are bad laws. And circumventing bad laws is good for society.

Paying an undocumented immigrant to mow your lawn, clean your house, or watch your kid is illegal. But it is also a mutually beneficial exchange with no obvious externality. If taxing supernotes discourages these kinds of transactions, society is worse off than it otherwise would be.

The stakes are even higher for those living under repressive regimes. “Money is coined liberty,” Fyodor Dostoyevsky observed, “and so it is ten times dearer to a man who is deprived of freedom.” It might be illegal to bankroll an opposition newspaper or purchase supplies for a peaceful protest. But it is certainly not immoral. Indeed, to the extent that the proposed supernotes undermine illiberal governments, they should be subsidized—not taxed.

How about tax evasion? As I have explained elsewhere, the social costs of tax evasion, which stem mostly from the misallocation of resources, are relatively small. Moreover, there is an offsetting benefit to tax evasion: it limits the extent to which governments can overtax. Tax evasion, like circumventing unjust laws, is especially important for those living under repressive regimes. Supernotes would give citizens around the world a peaceful way to express their discontent with climbing tax rates—a way that their profligate governments would have no choice but to acknowledge.

Taxing supernotes is not a narrowly tailored policy to deal with the social welfare reducing criminals and tax cheats in our midst. Such a tax does not discriminate among users. It is akin to spanking all of your children when one of them misbehaves. Sure, the criminals and tax cheats are punished by the tax on supernotes. But all of the well-behaved users are punished too. And, as I have argued above, there would likely be a lot of well-behaved users.

The case against taxing supernotes at a higher rate is even stronger when one realizes that the tax on existing notes is already too high. As Koning points out, inflation is a tax on cash. And, as with any other tax, it prompts users to switch to less desirable alternatives to avoid the tax. That is a problem. If we are holding too little cash, we are less well-equipped to make transactions. Some transactions—and the gains from those transactions—will go unrealized as a result.

In a much-cited article, Milton Friedman argued that setting the rate of return on cash equal to the rate of return on risk-free bonds would induce people to hold the optimal quantity of money. Today, the real rate of return on a 1-month Treasury bill is around 0.45 percent. Hence, Friedman’s analysis suggests that the optimal tax on currency is not 2 percent, the Fed’s current inflation target, but something in the neighborhood of negative 0.45 percent.

Koning’s proposal to issue supernotes taxed at a higher rate than lower denomination notes is half right. The U.S. government should issue supernotes. A century of inflation under the Federal Reserve means that the largest denomination notes in circulation today can purchase a fraction of the goods they would have commanded a hundred years ago. To match the buying power of a $100 bill in 1918, we would need a note equivalent to around $1,714.21 today. The $500 and $1,000 notes proposed by Koning would go a long way toward bridging that gap. They would preserve the currency’s ability to promote financial privacy and offer refuge to those living under repressive regimes.

Taxing supernotes at a higher rate than lower denomination notes, however, is unwarranted. Indeed, there is a strong case for subsidizing all notes in circulation—setting the rate of return on cash equal to the rate of return on risk-free bonds, as Friedman recommended. Such a policy would not require cutting checks to users at the point of redemption. Rather, the Federal Reserve need merely commit to a policy of mild, productivity-driven deflation. Subsidizing notes in this manner would also negate the need to issue even larger denominations—super-duper notes—in the future.

The Conversation

The Harm of Tax Cheating

Before I begin my response I’d like to thank James McAndrews, Josh Hendrickson, and Will Luther for participating in this conversation, I very much enjoyed reading their responses.

While Luther and McAndrews provided qualified support for the idea of adding a new high denomination U.S. note, all three commentators push backed against the idea of having it depreciate so that an extra tax is placed on supernote owners.

There are several technical and fundamental criticisms. On the technical side, McAndrews questions whether the monetary authority’s stipulated redemption rate will pass through to end users of currency, especially given the fact that banknotes are traded in decentralized markets.

Central banks often cancel, or demonetize, various denominations of banknotes. Sweden recently demonetized the 1,000 kronor banknotes because they lacked strong anti-counterfeiting measures, replacing them with a new issue. A more notorious example is India’s sudden demonetization of its 1,000 and 500 rupee notes. I’d argue that each reduction in the redemption rate for supernotes is similar to a demonetization, the difference being in scope: in the latter case the central bank annuls the entire value of a note whereas in the former it annuls just part of it. We know that demonetizations are generally passed through to decentralized banknote markets. Neither the old Swedish 1,000 kronor nor either of the two Indian demonetized notes continues to circulate. If the market listens to demonetizations, it seems like it would do the same with a tax.

Turning to non-technical criticisms, Luther and McAndrews both point out that a supernote tax would penalize not only those engaged in noxious activity but also those who use the note for good purposes.

I think this characterization is right, but it seems no different to me than other markets on which society has deemed it appropriate to levy a corrective tax. Take the alcohol market. Heavy alcohol users can impose a number of costs on society including family problems, assaults, intoxicated driving, and vandalized property. At the same time, there are many responsible drinkers who benefit from the occasional glass of wine. While the existence of good uses for alcohol complicates the social welfare calculation, it doesn’t mean that the alcohol market should not be taxed. The economic distortions imposed on responsible drinkers by the tax are presumably outweighed by the benefit of having heavy drinkers bear the costs of the damages they impose on others. A tax on supernotes would work along the same principles.

Hendrickson questions whether the sorts of activities enabled by supernotes qualify as externality-generating. Pollution is a text-book externality, says Hendrickson, since it causes genuine health and productivity problems. The illegal activity facilitated by banknotes might annoy others, he points out, but this distaste isn’t the sort of externality that society generally tries to correct for.

This is probably true of many illegal activities enabled by cash, such as prostitution. Observers might find the activity abhorrent, but they do not suffer physical harm from it. However, it seems to me that tax evasion abetted by banknotes is more than just distasteful; it hurts other tax payers. To keep up the same level of government spending, the “suckers” must make up for the cheats by paying more than their fair share.

Luther minimizes the costs of tax evasion, referring to an article in which he describes tax cheating as a “mere” transfer. According to Luther, the government is made worse off, but tax cheats are better off, so in a social welfare calculation the two effects offset each other.

I’m not convinced that the arithmetic used to account for tax cheating can be reduced to a simple transfer. Let me turn to an analogy. Imagine that some sort of broadly available financial technology allowed people to easily steal from Wal-Mart and other retailers. We might describe the jump in theft that Wal-Mart suffers as a mere transfer, the thieves benefitting to the degree that Wal-Mart shareholders lose. But we would also worry about the damage that this theft-enabling technology does to the institution of property rights. If there is a general reduction in society’s sense of quid pro quo—the idea that a solid day’s work leads to a solid day’s pay—then an economy can’t function as well as it should.

In the same way that the theft-enabling technology hurts the institution of property rights, cash-based tax evasion damages the delicate balance that keeps a well-designed tax system functioning. Without a sense of quid pro quo, would-be taxpayers may simply choose to become cheaters.

Luther also mentions that the rate of return on cash should be boosted so that it yields the same rate as a risk-free bond, as suggested by Milton Friedman. I am sympathetic to this idea but would prefer to limit the application of the Friedman rule to low denomination notes, as they are more likely to be used for licit transactional purposes. So for example, $1s, $5s, and $10s would all bear interest while supernotes would continue to have a negative rate of interest applied to them.

Finally, Luther’s calculation for the amount of illegally used U.S. banknotes points to the inadequacy of data being used to guide this discussion. While it is certainly difficult to collect information about underground usage of banknotes, one hopes that central banks will make more efforts in this direction given the growing importance of questions about financial privacy.

Who Uses High-Denomination Notes?

J. P. Koning wants to realize the benefits of larger denominations—supernotes—while limiting the corresponding costs from crime and tax evasion that such notes would encourage. To accomplish this, he has proposed issuing supernotes that are subject to a tax. The problem with his proposal, as James McAndrews and I explain in our initial responses, is that the tax is levied on all users—not just those involved in crime and tax evasion.

In a follow-up piece, Koning notes that the market for supernotes “seems no different […] than other markets on which society has deemed it appropriate to levy a corrective tax.” He is certainly right in one respect: real-world corrective taxes tend to punish the good and bad alike. But it does not follow that such a policy makes us better off, even if “society has deemed it appropriate” (whatever that means).

Who is using large denomination notes? That is the relevant question in my mind. To see why it matters, let’s consider two somewhat extreme scenarios:

- Large denomination notes are primarily used by law-abiding citizens.

- Large denomination notes are primarily used by criminals and tax cheats.

We will also ignore the complications of welfare-improving criminals and tax cheats that I raised in my earlier response. Instead, we will assume all crime and tax-cheating is bad for society on net, and all law-abiding transacting is good for society on net.

In the first case, issuing supernotes would seem to be a good idea. Society gets all of the censorship resistance, data protection, and global back-up monetary system benefits that Koning wants at a relatively small crime and tax evasion cost. However, in this scenario, there would also seem to be little scope for improving matters with a tax on supernotes. The tax, which does not distinguish between the two user groups, mostly falls on law-abiding citizens because—by assumption—they are the primary users of large denomination notes.

In the second case, levying a tax on supernotes would seem to be a good idea. The tax mostly falls on criminals and tax cheats because—again, by assumption—they are the primary users of large denomination notes. However, in this case, it is no longer clear that supernotes should be issued at all: society incurs a large crime and tax evasion cost for little censorship resistance, data protection, and global back-up monetary system benefit.

I have focused on somewhat extreme scenarios. Perhaps the real world falls somewhere in between. But the general point remains. If the benefits of issuing supernotes are large, there is probably little scope for improving matters with a tax. If issuing a tax on supernotes improves social welfare, it is probably a bad idea to issue supernotes in the first place.

Some caveats are in order. For one, it might be the case that law-abiding citizens are much less sensitive to the tax than criminals and tax cheats. If so, much of the crime and tax evasion can be discouraged without losing the benefits realized by law-abiding citizens. Additionally, the link between user group shares and the costs and benefits of issuing supernotes might be weaker than I have suggested. A few criminals might impose very large costs on society in the first case. Similarly, a few law-abiding citizens might realize very large benefits for society in the second case. Nonetheless, for many parameterizations of this simple model, the point remains: we cannot have our cash and eat it, too.

Finally, I take issue with the implication that a prevailing policy is good because “society has deemed it appropriate.” For one, it is not obvious that society has deemed a policy appropriate simply by virtue of observing that the policy has prevailed. One can only say for certain that the policy has survived the political process. Whether that policy maximizes social utility depends on a host of institutional details. It might be the result of concentrated benefits and dispersed costs. Or, it might be the case that society has deemed a bad policy appropriate due to rationally irrational behavior: the members of society, to paraphrase H.L. Mencken, know what they want and deserve to get it good and hard. Some prevailing policies are good. Some prevailing policies are bad. We cannot judge policies based solely on their having prevailed.

High-Denomination Notes That Stop Crime

One of the main topics of our discussion has been the fraction of law-abiding citizens who would hold the new “supernotes” and the corresponding welfare effects. I think that this issue is important, but not for the reasons that have so far been discussed. My primary motivation is to discuss the idea that the fraction of law-abiding citizens who use the notes is endogenous to the “supernote” tax proposal.

In assessing the costs and the benefits, J.P. Koning noted that alcohol taxes do not discriminate based on the behavior of the purchaser. The implication seems to be that it is okay to tax both good and bad actors as long as the benefit of the reduction in “bad” behavior is greater than the cost of the reduction of “good” behavior. To determine whether the supernote tax policy provides a net benefit, we would need to determine the fraction of law-abiding individuals holding supernotes, the fraction of criminals holding supernotes, and their respective sensitivities to the tax. Will Luther countered that either the supernotes provide a social benefit and shouldn’t be taxed, or that supernotes should not be issued at all. The trouble I have with this debate is that the fractions of the respective groups holding the supernotes are not something that can simply be taken as given. In reality, the fraction of each group is a function of the size of the tax. In fact, the success of Koning’s supernote proposal seems to completely rely on this point.

Consider a textbook example of social cost. Suppose that there is a factory that pollutes a river. Downstream from the factory is a fishery. If the fishery owns the rights to the river, then this pollution is a violation of its property rights. The factory could pay the fishery for the right to pollute the river, provided the compensation is sufficient to offset the costs of the pollution. In the absence of significant transaction costs, this is what we would expect to happen given the initial distribution of property rights. In my last essay, I pushed back on the idea of illegal trade as necessarily fitting the definition of an externality. Nonetheless, if we accept the premise that illegal trade generates some sort of social cost, then there should be a similar solution to this problem. For example, criminals might be willing to pay law-abiding citizens to ignore the illegal activity. If the payment is sufficient to offset cost imposed on law-abiding citizens, then law-abiding citizens will be sufficiently compensated.

Of course, practically speaking, we should not expect this to occur in reality. The reason is that criminals tend to hide their activity. We would therefore never expect a group of criminals to come forward, volunteering their identities and their role in illegal activity, and offer compensation to law-abiding citizens. Nonetheless, there might be a role for policy here. The role for policy can be seen from a mechanism design approach to the problem. In other words, we know the desired allocation, but we need to design a policy that reveals types in order to implement that allocation.

One policy that can potentially accomplish this goal is to introduce a supernote that circulates alongside traditional currency denominations, but earns a different rate of return. The varying rates of return are crucial. Since criminals are likely to prefer the use of supernotes, they will be willing to hold these notes at a lower rate of return than law-abiding citizens. It is therefore possible to vary the rates of return on traditional denominations of currency and supernotes to create a separating equilibrium. To put this another way, it is possible to vary the relative rates of return such that only law-abiding citizens hold traditional denominations and only criminals hold the supernotes. By having a positive rate of return on traditional denominations and a negative rate of return (a tax) on supernotes, policymakers can create precisely the type of transfer from criminals to law-abiding citizens described above.

This example highlights that introducing a supernote that is taxed need not have any effect on law-abiding citizens provided the tax is sufficiently large that only criminals decide to use them. Thus, contrary to Koning’s assertion, whether the policy is a good idea does not depend on the fraction of supernotes held by the respective groups. Also, contrary to Will Luther’s claim, the introduction of the supernote in this instance is welfare-improving (given the premise that illegal trade creates a social cost) because it allows policymakers to engineer a transfer from criminals to law-abiding citizens that would not be available otherwise.

Nevertheless, there is a caveat to this example. Criminals would prefer supernotes because of the high denominations. If the tax is sufficiently high, however, the cost will not be worth the benefit. With the term “sufficiently high,” the devil is in the details. The existence and the creation of alternative media of exchange will put a limit on the tax. If the tax is too high, criminals are likely to switch to traditional denominations, cryptocurrency, or even create their own payment system. To implement Koning’s proposed policy requires that policymakers are able to thread a needle. These policymakers need to implement a tax that is high enough to prevent law-abiding citizens from using it (thereby facilitating the transfer), but not so high that criminals will choose an alternative.

Monetary Technologies for the Unbanked

The discussion this month by J.P. Koning, Joshua Hendrickson, and William Luther has touched on many issues, too many to address here. I will discuss two difficulties that I see with J.P. Koning’s original proposal to introduce a high-denomination note in the United States and to tax it: First, what evidence do we have that a high-denomination note is needed? Second, is taxing notes of different denominations feasible?

To answer the question behind Koning’s proposal, namely, “Does the United States need a new note of $500 or $1,000 denomination?” requires an empirical investigation. Although the real value of the $100 note has declined over the last several decades as the moderate inflation experienced in the United States has whittled away at its purchasing power, alternative means of payment have been developed during that time. Paying by card or smartphone app is both common and incredibly convenient today, a marked change from a few decades ago. The development of convenient and near-universal electronic payment methods poses a fundamental challenge to the introduction of any new payment method, including a high-denomination note. To determine if a new high-denomination note would be in demand, we must assess the likelihood that it would be used in everyday commerce.

Many people, particularly those who lack bank accounts or smartphones, are poorly served by the modern card and smartphone payment methods. Many of those people are also poor and have highly uneven income. The financial system is not doing a particularly good job of providing them with convenient alternatives to currency. But would a high-denomination note help them? Carrying five $100 notes is only slightly more inconvenient than carrying a single $500 note, so I don’t believe that the provision of a high-denomination note would serve the unbanked’s demands much better than the current set of denominations. This conjecture is supported by survey evidence that most people, including the unbanked population, carry relatively little currency, and primarily of low denominations.

To pursue the proposal of issuing a high-denomination note, I’d first like to see a proposal to gather evidence that such a note would be used. Current surveys do not provide sufficient evidence of the need for a new note. Different types of surveys, such as marketing surveys, would be useful to provide better insight into the question of whether people would welcome the note and use it. For example, would corner grocery stores accept such a note in payment? Many stores currently limit the denominations they accept to a maximum of $20. I would expect that very few stores would accept a $500 note, but rather than speculating about this question, surveys can be designed to measure the potential response of store owners and consumers alike. We need more evidence before we can assess the potential uses of such a note.

The second concern I have with the proposal is its suggestion that the new notes be taxed. While both Koning and Hendrickson suggest ways to tax notes, William Luther and I have emphasized that the tax may fall on many law-abiding citizens as they would use the new notes. Even more fundamentally, I continue to doubt the ability of society to enforce such a tax.

While Koning likens a tax to various demonetizations of currency, reasoning that the demonetizations have feasibly achieved their goals, a tax on notes would seek to decentralize a much smaller reduction in value for notes on a frequently recurring basis. Differential taxation of notes of different denominations is similar to imposing different rates of inflation on the different notes. It would be difficult to communicate and enforce those different rates throughout the economy—stores would have to post the current daily rate of exchange for the high-denomination notes. Peter Garber suggested the best idea for imposing differential costs on note-holders, which was to increase the physical dimensions of high-denomination notes.[1] In that way, anyone who uses such a note is subject to the inconvenience of handling and storing the notes. This would be especially costly to those criminals engaged in the drug trade, who handle vast numbers of notes, and whose storage and handling costs of notes are a significant part of their overall costs of doing business. Although this idea would increase the costs of handling and storing notes, it is not a tax, and raises no revenue for the government. It does highlight, though, the importance of thinking through the details of exactly how a tax would be enacted.

One further objection to a taxed note is that, even were a tax to be perfectly enforced, the differential rates of exchange among the different denominations of notes is an inconvenience. The cost of all those calculations required to make change and set different prices based on which note a customer offers must be counted against whatever benefit a tax might achieve.

The development of card and smartphone methods of payment has been astounding. Those means of payment are convenient and provide many benefits, such as recordkeeping, that aren’t available with currency. These methods have largely substituted for currency as the real value of the U.S. currency’s fixed denominations has declined. However, they don’t replicate all the economic features of currency. Working on expanding the functions of electronic means of payment to mimic those of currency, such as improving privacy protections, is likely a better way to improve our monetary system than to introduce a new high-denomination note. In addition, society should take greater efforts to improve access to the financial system to poor and unbanked populations.

Note

[1] Peter Garber, “A Barbaric Relic,” Book Review, IMF Finance & Development,September 2016, Vol. 53, No. 3.