About this Issue

The U.S. Federal Reserve marks its 100th anniversary this year. Has it been worth it? Critics of central banking point to continued inflation for much of the Fed’s history, its tendency to become embroiled in politics, and the ever-present dangers of a fiat currency. Supporters counter that a commodity money would be no better and would in many ways be worse; they add that many of the Fed’s missteps, including mismanagement of the Great Depression, are unlikely to be repeated. Macroeconomic science really has progressed in the last 100 years, and central banking is a key part of that story.

Which side is right? This month we have invited four experts to discuss the pros and cons of central banking, starting with a lead essay by Cato Institute Senior Fellow Gerald P. O’Driscoll Jr. We will have responses by George Mason University Professor Lawrence H. White, Bentley University Professor Scott Sumner and former Cleveland Federal Reserve President Jerry L. Jordan.

Lead Essay

The Fed at 100

Ron Paul’s two runs for the Republican presidential nomination made “End the Fed” into a political slogan. Reportedly it was the line receiving the greatest applause at all his rallies, no matter the group. It was also the title of a book he authored. It is a sign of the times that the Fed is held in low esteem in its centennial year, more among the public than in academia.

Long before abolishing the Federal Reserve became a political cause, the idea of banking without a central bank developed as a serious topic of scholarship. It is to this scholarship that I will address my comments.

During my time as a research economist and later vice president at the Federal Reserve Bank of Dallas (1982–1994), ideas for monetary reform were in the air. We were still in an era of high inflation and emerging from recession and economic stagnation. The Gold Commission had issued its report in March 1982; I joined the Dallas Fed in October. The Federal Reserve was held in low esteem at the time as well, and those of us who spoke to the public were almost apologetic for where we worked.

Also in 1982, Arthur J. Rolnick and Warren E. Weber of the Federal Reserve Bank of Minneapolis wrote a famous paper, “The Free Banking Era: New Evidence on Laissez-Faire Banking.” It was a revisionist account of the U.S. free banking era, casting free banking in a more favorable light than in textbook accounts. At a Fed conference, Art told me that he thought it was an open question whether we needed a central bank. He later rose to become Senior Vice President and Director of Research at the Minneapolis Fed. I leave it to the reader to consider the irony of a central banker writing favorably about a banking system without a central bank.

Economic historian Hugh Rockoff had already written “The Free Banking Era: A Re-examination” in 1974. As its title suggests, it also treated the U.S. free banking era more favorably than did the textbooks of the time. Other important work was also done within the Federal Reserve System, including the work of Gary Gorton at the Philadelphia Fed.

The watershed event in the free banking literature was the 1984 publication of Lawrence H. White’s Free Banking in Britain: Theory, Experience, and Debate, 1800–1845. The book, based on his UCLA Ph.D. dissertation, examined the Scottish system of free banking. That system was a purer form of free banking than the U.S. system. The Scottish system developed and flourished from 1695 to 1845. The system did not fail but was legally suppressed by the Bank Acts of 1844 and 1845. Those acts solidified the privileged position of the Bank of England.

A great deal of research has been conducted since, appearing in articles too numerous to cite and written by authors too numerous to identify here. I will reference one important recent paper by George Selgin, William Lastrapes and Lawrence H. White, “Has the Fed been a failure?” which appeared as part of a symposium in the Journal of Macroeconomics (2102): 569-596. The authors re-examined the empirical literature on the Fed’s performance from 1913 to the present and compared it to that of the National Banking System, which preceded it. The literature has come to view the Fed’s performance, even excluding the Great Depression, less favorably, and the performance of the National Banking System more favorably. The authors argue the evidence now tilts in favor of the pre-Fed area.

This posting appears right after an important conference held at the Mercatus Center on November 1st on “Instead of the Fed: Past and Present Alternatives to the Federal Reserve System.” Important new research was presented there. And, of course, the 31st annual Cato Monetary Conference will be held at the Cato Institute on November 14th. Further research on free banking and central banking will be presented there. I can also report that the 2014 meetings of the Association of Private Enterprise Education in Las Vegas, April 13th to 15th will include more research comparing the performance of the monetary system pre-Fed and post-.

The literature on free banking demonstrates the viability of private, competitive banking without a central bank. That viability is demonstrable even though free banking systems differed greatly from each other. Vera C. Smith (later Vera Lutz) wrote a dissertation under Friedrich Hayek titled The Rationale of Central Banking (1936). She described the antebellum U.S. banking system as “Decentralisation without Freedom”: The substantial regulation on banks belied the word “free.” Instead, the system was fragmented with many small, undiversified banks. (The book is currently in print from Liberty Fund.)

The post–Civil War National Banking System was anything but unregulated. Importantly, banks were national only in the sense of having federal charters. They lacked the ability to operate across state lines or even to branch within states. Still more importantly, they were restricted to using U.S. government debt as collateral for note issue. Despite all the regulatory hobbling, the National Banking System functioned, and by some accounts as well or better than the current system. There was enough competition to stimulate banks to innovate around the restrictions, for example by developing deposit banking.

Free banking was certainly viable under the classical gold standard. The strongest argument against central banks in a classical gold standard is that they serve no purpose. Central banks perform no essential function in a commodity money system. That has been recognized by many economists, perhaps most notably Alan Greenspan.

Does the literature make an intellectual case for ending the Fed? The 19th century economic journalist and Economist editor Walter Bagehot thought it would have been better if the Bank of England had never been created. In Lombard Street, Bagehot argued that a decentralized system of many banks of approximately equal size would have been preferable. Instead of reserves being concentrated at the Bank of England, reserves in the competitive system of banking would have been dispersed among all banks.

Concentrating reserves at a central bank was the cause, not the cure, for panics. The concentration of reserves exposed the banking system to periodic panics and scrambles for liquidity. Bagehot’s famous dictum that Bank of England must lend freely at penalty interest rates in times of panic was a second-best solution to a problem caused by centralizing reserves in that institution.

Having said that, Bagehot argued that, once created, it was not possible to abolish central banking. His argument invoked the high costs of institutional change, which cannot be denied even today. Before taking Bagehot’s argument at face value, however, we should examine the costs of keeping the current system. I will argue that the costs of central banking are higher than they were in Bagehot’s time. They are higher because we have a fiat money standard now.

While I have pointed out that central banks are unnecessary in a classical gold standard, they probably did not do a great deal of harm. They were constrained in their discretion. They did “sterilize” reserves, which means they resisted letting the domestic money supply respond automatically to changes in gold reserves. Central banks could not do so for prolonged periods, however.

Before proceeding further, I will examine the question of why central banks came into existence if they were unnecessary from the perspective of sound monetary policy. The writings of the classical economists point us to the answer, which was clear already by the 18th century. Adam Smith observed that monarchs were in a chronic state of impecuniousness. In peacetime sovereigns spend their entire revenue, and then some, on “every sort of expensive luxury.”

Sovereigns were also prone to engage in wars either to extend their dominion or to defend it. In the era in which the modern nation state arose, Smith argued that “The want of parsimony in time of peace, imposes the necessity of contracting debt in time of war.” Sovereigns borrowed to finance wars until their credit dried up. Then they turned to various expedients. They sold monopolies; made arrangements with guilds; seized Church lands and revenues; and appropriated the property of Jews and expelled them. The most frequent expedient was for the king to “clip” coins and debase them. But each of these practices led to inflation. All of them came before central banking, which was not even a concept in the 17th century.

The rise of central banking was an unintended consequence of kings’ fiscal problems. It was not invented but evolved to solve those problems. There was no thought of anything that we would call monetary policy today. In England, Charles II spent and borrowed heavily until he defaulted on his loans to bankers. Later, in Vera Smith’s words, William III “fell in with a scheme” to raise 1,200,000 pounds (a princely, or I should say, kingly sum in that time). Legislation created the Bank of England in 1694, which was authorized to raise that sum in capital and immediately lend it out to the king.

Between 1694 and the beginning of the 19th century, the pattern repeated: the bank’s charter was extended and more capital was raised and lent to the government, with the consequence of more Bank of England notes outstanding. In 1697, the Bank was granted the privilege of limited liability for members of the corporation. That privilege was denied to all other banks for another century and a half. And, in 1812, the Bank’s notes were granted legal tender status, solidifying its monopoly position.

The Bank of England became a central bank because of its monopoly status. That status evolved over time in a piecemeal fashion with no thought of the ultimate consequence. Fiscal considerations drove the process over more than a century. The details of the story vary for other countries, but spending and deficits typically drove the process.

The creation of the Federal Reserve was a notable exception. The United States’ fiscal house was in order, but the restrictions on the National Banks made them prone to periodic crises of two kinds. One was seasonal following the agricultural cycle. At harvest time, farmers needed currency to pay workers. Country banks kept reserves with city banks, and the former drew down their balances at the latter institutions. The restrictions on collateral for currency meant that the supply could not increase with an increase in demand. That was a design defect of the system, well understood at the time. Politics blocked reform.

The seasonal changes in the demand for currency in rural areas were thus transformed into credit stringency in cities and even the major money centers like New York and Chicago. There were predictable seasonal mini-crises. None of this was inherent to private money issuance, but a consequence of legal restrictions.

Maxi-liquidity crises occurred less frequently but were more dramatic. They typically were the result of some kind of real shock either in the United States or abroad. The Panic of 1907 was particularly severe. The details are not important, only that the Panic led to calls for a permanent solution. In other political environments, it might have led to a reform of the National Banking System. I believe that would have been preferable. But the early 20th century had seen the rise of Progressivism in both the Republican and Democratic parties.

In the aftermath of the crisis, Progressive forces aligned with big banking to devise a strategy for creating a central bank. Each group had its reasons for wanting a solution involving greater federal government control over banking, and at times it was difficult to distinguish the two groups. Neither wanted greater freedom or more competition in banking as a solution. In the Triumph of Conservatism, Gabriel Kolko chronicled the sequence of events.

What became the Federal Reserve Act was first developed by Republican Senator Nelson W. Aldrich of Rhode Island, the Senate being under Republican control. It was done under the guise of the congressionally created National Monetary Commission. A Democratically controlled Congress eventually passed a bill and it was signed into law by Woodrow Wilson in 1913. That bill was more like than unlike the Aldrich proposal.ld. There have been numerous sessions at professional meetings and a number of conferences examining the 100-year history of the Federal Reserve. What has been missed in these events, at least at those with which I am familiar, is that the Fed’s creation was a crowning achievement of the Progressive Wilson Administration.

I now fast forward to FDR’s taking us off the gold standard domestically, which also involved a default on gold-backed Treasuries. The Federal Reserve overnight went from managing a modified gold standard to being responsible for controlling a fiat money system. It soon precipitated another recession, that of 1937–38. Wartime finance then made monetary policy explicitly and totally subservient to fiscal policy.

Only the end of the Korean War tested the Fed’s capacity to manage a fiat money system. Here I am going to draw from my paper for this year’s Cato Monetary Conference, “The Case for Monetary Reform.” Let us consider a roughly sixty-year period of managing fiat money. There were two periods in which the Fed produced reasonably stable monetary policy: the decade of the 1950s and a period known as the Great Moderation (the mid-1980s to the mid-2000s). Together, they are roughly 30 years, or half the period. From the mid-1960s through the 1970s, monetary policy was increasingly bad as the inflation rate first edged up and then galloped. The phenomenon of “stagflation” emerged: inflation and recession simultaneously. High inflation continued into the 1980s. That entire period was the Great Inflation and lasted roughly 20 years, or one-third of the period. The Great Moderation, also lasting about 20 years, ended in the great Housing Boom and Bust.

In short, the record is unenviable.

The Great Moderation occurred against a background of large budget deficits that declined first as a percent of GDP and then absolutely. The decade of the 1950s was one of low deficits or even an occasional surplus. When the Kennedy and Johnson Administrations started engaging in fiscal activism under the sway of Keynesianism, the Federal Reserve under Chairman William McChesney Martin monetized the resulting deficits.

The two episodes illustrate that there is fiscal dominance: Fiscal policy forces the hands of central bankers, and they accommodate loose fiscal policy. We consider central banking modern, but it ultimately accomplishes more efficiently what sovereigns did by clipping coins and debasing the currency. As Adam Smith taught us, governments are prone to overspend and must borrow. Yearly deficits accumulate into unsustainable debt levels. At some point, governments come to depend on monetary instruments or policies that allow them to reduce the real value of that debt through inflation. Wars drove deficits in the 18th century. For most developed countries today, the welfare state does so instead.

The gold standard made chronic budget deficits impossible. Indeed, the U.S. experience was one of peacetime surpluses, which were used to pay off wartime deficits. With fiat money, there is no such constraint on deficits, and classical fiscal theory has been thrown out the window. Central banking with fiat money enables governments to run large deficits. That makes it more costly than when Bagehot considered the issue.

No large, modern government could operate without a central bank. Abolishing central banks would require first downsizing governments and their appetite for resources to fund war and welfare. I certainly support doing so. I am suggesting, however, that consideration of abolishing the Federal Reserve involves a great deal more than monetary policy.

The Cato Institute has a plan for downsizing government, and I recommend that interested readers consult it (www.downsizingovernment.org). For our purposes, let us assume that it will be implemented. Could we then end the Fed?

I don’t know any successful examples of free banking with fiat currency. There must be a constraint on competitive banks, or they will over-issue liabilities. Commodity standards inherently provide such a constraint, along with the rule of law and its requirement to honor contracts (especially to honor promises to pay out specie on notes and deposits).

There are proposals to freeze the monetary base as a prelude to free banking, but it would not be as effective a constraint as a commodity standard. Congress could, for instance, pass a law freezing the monetary base. But no Congress can bind a future Congress. True, Congress could undo a gold standard, but changing fundamental institutions is more difficult than altering the wording of an ordinary statute.

Accordingly, I am not sanguine about proposals to mix fiat money and free banking. I have argued elsewhere that competitive banking requires a return to a commodity standard. I haven’t changed my mind, but am always open to being proved wrong.

In sum, downsize government and return to a gold standard, or come up with an alternative, effective constraint on money creation. Then we could discuss seriously whether to end the Fed. If that is the goal, a good deal more work must be done on planning and implementation. In “The Case for Monetary Reform,” I propose a strategy for those interested in this or some other monetary reform.

Response Essays

The Fed’s Track Record

Jerry O’Driscoll’s wide-ranging lead essay valuably introduces several important themes for discussion. I will here examine in more detail the historical record of the Federal Reserve System. The examination validates O’Driscoll’s characterization of the Fed’s record as “unenviable.”

The Federal Reserve Act was passed in December 1913. The Act did not assign the Fed any responsibility for monetary policy, because the gold standard was supposed to continue to govern the quantity of money in the U.S. economy. The twelve Federal Reserve district banks were expected only to be adjuncts to the banking system (bankers’ banks, lenders of last resort, and regulators of their member banks), and the Board of Governors basically an oversight body. The act did empower the Reserve Banks to issue banknotes, but it did not exclude the continued issue of notes by commercial banks, and it placed a 40 percent gold reserve requirement against Federal Reserve notes in circulation.

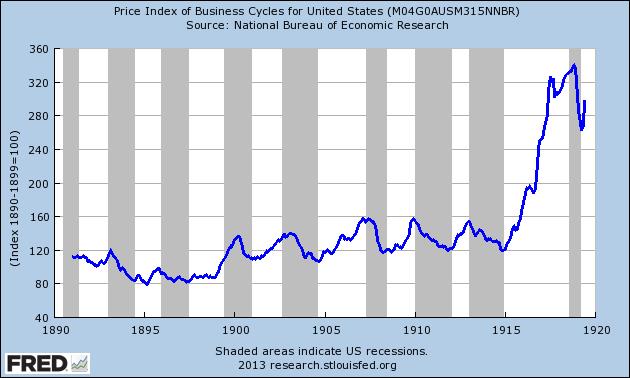

The Act’s framers did not foresee that World War I would fatally wound the gold standard. The War got underway in Europe in June 1914, just before the Federal Reserve Banks began operations in November. European combatant nations soon suspended the gold standard in their own economies, and much gold flowed from Europe to find safe haven in the United States. These developments removed, for the time being, any binding gold constraint on money creation by the Fed. The Fed soon began creating money copiously to purchase Treasury securities and thereby help finance the U.S. government’s war mobilization. By the time the United States entered the war in April 1917, inflation in the United States (year-over-year change in the monthly Consumer Price Index) had already reached double digits. The inflation rate hit 20% by the end of the year. The Great War ended in November 1918, but U.S. inflation continued apace, peaking at a remarkable 23.7 percent rate in June 1920.

The wartime inflationary boom was followed by a sharp contraction, a deflationary recession, in 1920-21. According to NBER dating, the recession in real economic activity ran from January 1920 to July 1921. The month-over-month inflation rate turned negative in July 1920 and did not become positive again for two consecutive months until October-November 1922. The Fed had overseen a wartime inflation so great – unlike any under the pre-Fed classical gold standard – that the swing from inflation to deflation was unprecedented: From July 1919 to July 1920 the price index rose 23.7 percent, and over the following twelve months fell 15.8 percent.

The standard CPI series does not go back before 1913, but the dramatic destabilization of the price level brought by the Federal Reserve Act plus the Great War can be seen in Figure 1, which charts the dollar price of a bundle of ten industrial and agricultural commodities.

Figure 1

The Fed’ second decade produced only moderate positive to mildly negative rates of inflation up to 1930, but then came a period of sharp deflation during 1930-33, reaching a 10 percent annual deflation in 1932. A recent study by Sandeep Mazumder and John H. Wood (Economic History Review, February 2013) views this as the final wringing out of the Fed’s WWI inflation. The period was also of course characterized by huge swings in real activity, from the boom of the Roaring Twenties to the depths of the Great Depression. Austrian critics have plausibly blamed the Fed for over-stoking the boom by holding interest rates too low before 1929, making a crash inevitable. In their celebrated Monetary History of the United States, 1867-1960, Milton Friedman and Anna J. Schwartz pointed out that the Fed, having nationalized the roles previously played by clearinghouse associations, particularly the lender-of-last-resort role, did less to mitigate the multiple banking panics of the early 1930s, with their sharply deflationary and depressive effects, than the clearinghouses had done in earlier panics like 1907 and 1893. They concluded with good reason that the economy would have suffered less if the Fed had not been created.

During the Second World War, the Fed was again drafted into providing inflationary finance. As Robert L. Hetzel and Ralph F. Leach have noted (Federal Reserve Bank of Richmond Economic Quarterly, Winter 2001), “In April 1942, after the entry of the United States into World War II, the Fed publicly committed itself to maintaining an interest rate of 3/8 percent on Treasury bills,” which meant expanding credit as much as necessary. This time the inflation rate peak was 19.7 percent in April 1947. When the Fed sought to let the T-bill rate rise in 1947, “the Treasury adamantly insisted that the Fed continue to place a floor under the price of government debt by placing a ceiling on its yield.” Finally unshackled from this commitment by an “Accord” with the Treasury in 1951, the Fed from 1951 through 1964 kept inflation consistently low. But that didn’t last. In the mid-1960s, the Fed kicked off the peacetime Great Inflation by beginning to play the Phillips Curve, that is, trying to reduce unemployment by inflationary monetary expansion. Once job-seekers and employers stopped being fooled by inflation, the unemployment rate rose along with the inflation rate in the 1970s. (That “stagflation” episode could be profitably studied by those in the current Fed who seem to think that the inflation rate will not rise so long as unemployment and excess capacity measures remain high.) When financial market participants began driving up nominal interest rates to offset the shrinking purchasing power of the dollar, the Fed responded by trying to drive down interest rates with even easier money, which only threw more fuel on the fire. The inflation rate (CPI year-over-year) peaked at 14.8 in April 1980.

In the Great Moderation of 1985-2005, the Fed returned to lower inflation, and some commentators concluded that this time the Fed had finally learned how to manage a fiat money. Alas, again it didn’t last. The Fed had begun fueling an unsustainable housing boom by holding market interest rates too low for too long from 2001 to 2006 (at least as judged by the common diagnostic of the Taylor Rule). The consumer price index did not rise rapidly, but house prices (excluded from the CPI) did. We are still living with the fallout from the crash.

Since the crash the Fed has pursued an unconventional policy of near-zero nominal interest rates (negative rates in real terms) through the combination of “Quantitative Easing” and interest on reserves. Beginning in November of 2008, the massive bond purchase programs QE1 and QE2 have tripled the monetary base (the Fed’s own monetary liabilities), giving the banking system massive excess reserves. Yet money held by the public, measured by M1 or M2, has remained on a gradual growth path. The Fed deliberately neutralized the injection of reserves by paying banks interest to hold the excess reserves rather than lend them out and expand the broader money supply.

What was the point of the bond purchases, if not to expand the money supply? The point was credit allocation: in QE1 the Fed bought $1.25 trillion in mortgage-backed securities to prop up the price of those securities. The Fed also allocated hundreds of billions in funds to lending programs directed at specific sectors of the financial industry. Credit allocation is not part of monetary policy, nor is it part of a lender of last resort policy, but it is instead a cronyism policy, benefitting some businesses at the general expense.

To conclude, let me summarize the findings of the 2012 Journal of Macroeconomics article by Selgin, Lastrapes, and White that O’Driscoll cited. Compared to the pre-Fed classical gold standard period,

1) The Federal Reserve’s management of monetary policy has dramatically increased secular inflation. Over the pre-Fed gold-standard period of 1879 to 1914 the compound annual inflation rate was -0.05%. A bundle of goods purchasable for $100 in 1879 was purchasable for $99.95 in 1914. Over the most recent 50 years, From September 1963 to September 2013, the compound annual inflation rate was 4.14%. A bundle going for $100 in 1963 cost $761.54 in 2013.

2) In addition to raising the average inflation rate, the Fed has also increased price level uncertainty, whether measured by a rolling standard deviation of the quarterly price level, or by the conditional variance of extrapolative price-level forecast errors at 10-year and longer horizons. The result of greater uncertainty about the future purchasing power of the dollar has been the near-disappearance of long-term corporate bonds and a corresponding discouragement to long-term investment planning.

3) The Fed has not tamed the business cycle. It has not reduced real output volatility as measured by percentage standard deviation from trend. Output volatility over the Fed’s entire 100 years has been much greater than in the pre-Fed period. Even if we discard the Great Depression, real output during the post-WWII period has been no calmer than the pre-Fed period, despite the U.S. economy having become more diversified and less subject to supply shocks.

4) The Fed has not reduced unemployment. We shouldn’t expect it to, of course, but this implies that its “maximum employment” mandate is absurd.

In Defense of a Flexible Monetary Policy

Gerald O’Driscoll has written a provocative essay on the history of central banking and the advantages of moving toward a free banking regime. There is much I agree with in the essay. Free banking offers many advantages, and banking problems in earlier centuries were often caused by perverse regulations, not laissez-faire. The creation of central banking probably did more harm than good; indeed I believe O’Driscoll actually understates the damage:

While I have pointed out that central banks are unnecessary in a classical gold standard, they probably did not do a great deal of harm. They were constrained in their discretion. They did “sterilize” reserves, which means they resisted letting the domestic money supply respond automatically to changes in gold reserves. Central banks could not do so for prolonged periods, however.

In my view the sterilization of gold reserves by the major central banks was the primary cause of the Great Depression, and hence World War II.

I will focus on a few areas of disagreement.

- I believe O’Driscoll is overly pessimistic about the prospects for an improved fiat money regime. For instance I do not believe the “Great Inflation” of 1965 – 81 was caused by the monetization of fiscal deficits. The deficits were relatively modest during that period, and the national debt was falling as a share of GDP. Deficits became a much bigger problem beginning in 1982, but that’s exactly when inflation fell to much lower levels. Instead the Great Inflation was probably caused by a mixture of honest policy errors and politics.

- I believe O’Driscoll is overly optimistic about the effectiveness of gold standard regimes. In addition, I would argue that we should avoid policy regimes that are “tamper-proof.” We don’t know what sort of policy regime is best. Therefore we should have policy regimes that are easy to alter in a situation where they appear to be causing grievous economic harm.

In the late 1970s and early 1980s it was widely believed that fiat money regimes had an inflationary bias due to political pressure. I have doubts about whether this was the primary cause of the Great Inflation; it seems plausible that central bankers also had a flawed model of the economy. After all most academic economists (presumably free of political pressure) were making the same sorts of mistakes during the 1960s and 1970s.

During the 1980s and 1990s two things happened. Academic economists finally understood that central banks determine the trend rate of inflation, and central banks were given greater independence, either tacitly or officially. Under this new fiat money regime the inflation rate became well-anchored, and central banks no longer seemed swayed by political pressures. Indeed it’s remarkable that inflation in both the United States and the eurozone is running below the 2% target, despite high unemployment and significant debt problems.

Nor does this seem likely to change in the near future, as investors forecast low inflation for years to come. Once modern central bankers figured out the “Taylor Principle,” the so-called inflationary bias of fiat money seemed to mysteriously vanish. There are still plenty of problems with our monetary regime, but high inflation does not seem to be one of them.

O’Driscoll briefly discusses the possibility of combining fiat money and free banking. He ends up concluding that this sort of regime would be too susceptible to political tampering. In my view that’s a powerful advantage of a fiat money regime. Throughout history there are many examples of rigid monetary regimes that went seriously awry and caused great damage before they collapsed. In the early 1930s prices fell sharply under an international gold standard regime. Countries did not begin recovering from the Depression until they abandoned the regime. Argentina suffered from falling prices and nominal GDP in the late 1990s and early 2000s under a rigid “tamper-proof” currency board.

In the end both the United States and Argentina abandoned their highly flawed monetary regimes and recovered from their depressions. But in each case the depression was wrongly blamed on free-market capitalism and the political system reacted by enacting highly counterproductive statist policies.

In many respects the eurozone of today is an even more “tamper-proof” monetary regime than a gold standard or currency board regime. It is extremely difficult for an individual country to exit the euro without triggering a collapse of their banking system. The euro is much more than a fixed exchange rate regime. The peripheral economies of the eurozone certainly would have sharply devalued their currencies if they had been able to do so.

None of this is to deny that these historical examples are highly complex. Monetary policy wasn’t the only problem, other policy errors occurred. Interwar policymakers looked back at the hyperinflation of the early 1920s and the Argentine policymakers looked back at the hyperinflation they experienced under floating exchange rates during the 1980s. Both had good reasons to want to avoid devaluation.

So then it becomes a judgment call. How bad are the future mistakes under fiat money likely to be? And how bad might things end up under a rigid monetary regime such as a gold standard? In my view the downside risks from a return to a gold standard, however constituted, are far greater than the risks of persevering with fiat money and trying to make incremental improvements.

It has been argued that a gold standard regime combined with free banking would tend to produce a relatively stable monetary environment, usually defined as either stable prices or low but stable growth in nominal GDP. I do not share this optimism. I would point to research on the “Gibson Paradox” of the classical gold standard. Studies have shown that fluctuations in the real interest rate led to changes in the real demand for gold that largely account for fluctuations in the price level. When real interest rates fall the demand for gold rises, as the opportunity cost of holding gold decreases. Because the supply of gold grows at a relatively slow and stable rate, fluctuations in the demand for gold largely explain price level fluctuations in the period up until 1940.

The basic problem is this; neither individuals nor banks have an incentive to adjust their demand for gold in a way that would stabilize prices or nominal GDP. Assume global real interest rates fell close to zero due to an investment bust. That would sharply increase the demand for gold. Suppose that at the same time rapid economic growth in a continent with 60% of the world’s population (and a strong cultural affinity for gold) led to soaring nonmonetary demand for gold. If both of those things happened at the same time the real value of gold would soar dramatically higher. Any country with a currency fixed to gold would suffer severe deflation, as the price level is inversely related to the value of money.

Of course this hypothetical is exactly what happened in the past decade. And there is nothing about free banking that would prevent that sort of disturbance in the global gold market from causing severe price level fluctuations. Even worse, wages and prices are much stickier than in the 19th century, meaning that even mild deflation can now cause a severe recession.

The counterargument is that fiat money regimes also performed relatively poorly in recent years. Interestingly, this poor performance did not show up in the metrics that fans of the gold standard might have expected. Inflation remained relatively well anchored, certainly compared to earlier decades. So then what lessons can we take from the recent failure of monetary policy?

The inflation targeting regimes of the so-called “Great Moderation” represented a significant improvement over both the gold standard and the unconstrained fiat money regime of the 1960s and 1970s. Progress is being made. Just as we learned useful lessons from the mistakes of the 1930s in the 1970s, I believe the policy errors of the last decade will lead to a further improvement in fiat money. There is rapidly growing interest among academics and even a few central bankers in nominal GDP targeting. If we had been following a policy of nominal GDP targeting (level targeting) in 2008, the recent recession would have been much milder.

Many libertarians are distrustful of fiat money regimes managed by bureaucrats. I share their distrust. But the solution is not to go back to a gold standard regime that might work, but that might also fail catastrophically, discrediting free market capitalism. Instead we should move toward a fiat money system where market forces determine the quantity of money and interest rates. For instance one promising free banking proposal by William Woolsey would have currency redeemable into nominal GDP futures contracts at a fixed price (equal to the policy target). Government would define the dollar and leave everything else to the private sector. With stable NGDP growth, there is less demand for fiscal “stimulus” to boost demand, or to give bailouts to failing companies.

Who Will Guard the Monetary Guardians?

“Do we really need the FR?” — Ronald Reagan, 1981[1]

Gerald O’Driscoll raises several questions that the American public and their elected representatives ought to be pondering as the U.S. central bank celebrates (?) its centennial. Regrettably, the first question many people may have is “What is the Fed and what does it do?” An excellent recent John Stossel hour-long program is a great contribution to the task of educating ordinary people about our central bank.

Of course, even people who know something about central banking may be asking themselves “Can an advanced country in the 21st century have a stable, reliable banking system without a central bank?” O’Driscoll points them to literature about places and times where countries, including the United States, did not have a central bank. Specifically, there is considerable scholarly research into the varieties of what is generically called “free banking,” which is not the same as “unregulated, unsupervised wildcat banking” that is probably still taught in high school American History classes.

O’Driscoll addresses the question, “Why do we even have central banks?” by briefly summarizing the episodes in history in which governments got themselves in a fiscal bind and needed more cash to spend than the tax system would raise, so having a central bank with a printing press came in handy. For the past few centuries central banks certainly have been more efficient in ballooning the money supply and creating inflation than in Roman times when melting down gold and silver coins and adding in some lead was the preferred method.

However, O’Driscoll does note that the fiscal needs of government were not the original reason for creation of the Federal Reserve System a century ago. Basically, the United States had an archaic banking regulatory structure that had left the country with thousands of small, often unit, banks that were subject to bouts of illiquidity, bank runs, insolvency, and failures. Because of the political impossibility of reforming and modernizing the private banking system, Congress created a system of twelve regional “bankers’ banks” that were intended to bring stability to the volatile private banking system. At the time, the chief architect of the Federal Reserve, Congressman Carter Glass of Virginia, claimed that the Federal Reserve was not a central bank because we were on the gold standard and did not have the authority to create money.

Probably the most challenging question raised in O’Driscoll’s essay is the following: “What are the risks of doing nothing?” Currently, the U.S. inflation rate is reported to be quite low, so it is hard to get people to think much about the dangers of central banking. For the many people who think, “If it ain’t broke, don’t fix it,” O’Driscoll draws the connection between budgetary deficits and the national debt. At its root, monetary policy is a fiscal instrument in a fiat currency world. The power to create money is the power to tax, because inflation is merely a form of taxation. It is a regressive tax—it hurts lower income people more than the rich—it is a dishonest tax, and it strains the social fabric of nations. Nevertheless, throughout history it has been politicians’ preferred form of taxation.

In economics, the true burden of taxation is whatever the government spends. All current expenditures of government as well as promises to spend in the future must be paid: (1) out of current tax receipts; (2) out of future tax receipts—budgetary surpluses; or (3) via the implicit tax of debasing the currency through inflation.

Politicians find it difficult to restrain government spending, they know the voters do not like broad-based tax increases, and perpetual deficits are both unpopular and create economic distortions that make us poorer. As a consequence, the very existence of central banks with the power to buy the government’s bonds with newly created money causes moral hazard in other institutions of government. Even when it is widely understood that sluggish economic growth reflects perverse taxation and regulatory policies of government, politicians find it irresistible to attempt to correct the mistakes of the rest of government by printing money.

As O’Driscoll points out, when monetary systems are on a gold standard central banks cannot do great harm because monetary discipline is assured by the necessity to exchange surplus paper currency for gold. That limits the amount of money in circulation, so inflation is contained. However, once the link between the nation’s currency and gold or silver is severed, a crucial restraint on government spending is missing.

This point was well understood by James Madison. In drafting the Constitution, in considering what kind of monetary system the new country should have, Madison wrote,

It cannot be doubted that a paper currency, rigidly limited in its quantity to purposes absolutely necessary, may be equal and even superior in value to specie. But experience does not favor reliance on such experiments. Whenever the paper has not been convertible into specie, and its quantity has depended on the policy of the Government, a depreciation has been produced by an undue increase, or an apprehension of it.[2]

Later, Madison addressed the question of maintaining fiscal discipline if the country created a central bank with the power to create money, “But what is to ensure the inflexible adherence of the Legislative Ensurer to their own principles and purposes?”[3]

This is the essential question that must be answered. In the past century, all forms of institutionalized restraints on the size and scope of governments—limitations on their current expenditures and on their promises of future payments—have been tested and failed. Constitutions, treaties, statutes, and specie-standards for currencies have all been pushed aside, repealed, revoked, or simply ignored.

Proposals for answering Madison’s question range from simply trying again to put teeth into previous approaches, to bolder ideas that are new and even global. The challenge of institutionalizing discipline is not avoided by a simple “balanced budget amendment” to the Constitution. Politicians are at their most imaginative and creative when it comes to avoiding having to say “No” to constitutional limits on spending more money: Witness the fiscal messes facing state governments even though they are required to balance their budgets every year. Some ambitious ideas call for grand human design requiring major international consultation, cooperation, and even treaties. Less ambitious ideas would rely on the competition of human actions that would result from the end of central bank monopolies of currency.

Notes

[1] Ronald Reagan, handwritten note on correspondence he received from Gordon Luce while President of the United States, 1981. Reagan Library archives, FG 143033198.

[2] Padover 1953: 292; see Dorn 1988: 90–91] Dorn, J. A. (1988) “Public Choice and the Constitution: A Madisonian Perspective.” In J. D. Gwartney and R. E. Wagner (eds.) Public Choice and Constitutional Economics, 57–102. Greenwich, Conn.: JAI Press.

[3] Madison, James. Letter to Mr. Teachle, March 15, 1831.

The Conversation

No Rules Guiding Central Bank Actions

Last Thursday, November 14, two discussions about the policies and practices of the U.S. central bank were occurring only a few miles apart, but they may as well have been on opposite sides of the planet. In the U.S. Senate, a committee was questioning the nominee to become the next chairman of the Fed, while over at the Cato Institute’s Hayek auditorium scholars were looking back over the 99-year history of the Fed and pondering whether the future would be more of the same.

Neither discussion came to grips with the crucial issue of when and how the Fed eventually ends and ultimately unwinds its massive asset purchases, known as QE. What should “fed-watchers” be looking at to conclude that enough is enough, it is time to end “pedal to the metal” monetary actions? The Fed is backpedaling off the idea that there is a magic rate of unemployment that will signal the end is near. Scott Sumner suggests nominal GDP will signal when there is too much heat under the kettle. But then what? Nominal GDP jumped from 2.4% in QII to 4.7% in QIII, as the personal consumption price index went from a small decline in the second quarter to 1.9% increase in the third. Suppose NGDP rises further to 6% or higher in the fourth quarter? What should the FOMC instruct the trading desk to do? There is no Federal funds market; the Fed portfolio has no Treasury bills that can be sold.

My point is that there are no rules guiding central bank actions; there is no one inside or outside the Fed who can say anything meaningful about the future. Meaningful congressional oversight is not possible. Neither foreign exchange nor domestic bond markets are providing discipline. This cannot end well.

Good Compared to What?

The Fed: Good Compared to What?

I want to thank all those posting comments. I particularly want to thank the authors of the three other essays. I will respond to some points, and I will do so one author at a time. I have been delayed in doing so by a heavy travel schedule.

Professor White’s essay is an important addition to the discussion because he succinctly presents the historical record of Fed policy, making important comparisons to the pre-Fed record. I call everyone’s attention to his 4-point summation:

1. The Fed drastically increased inflation compared to the pre-Fed period.

2. The Fed increased price-level uncertainty.

3. The Fed has not reduced real-output uncertainty.

4. The Fed has not reduced the unemployment rate, which calls into question the whole idea of full-employment mandate.

Despite the historical record, there have been any number of papers written in the past year suggesting the Fed’s record is a good one. In light of White’s essay, I ask “compared to what?”

A Note on Bitcoin

A comment was posted on Bitcoin. This is a topic worthy of an essay unto itself, and the subject comes up in many discussions. Here is my take on it. “Money” is defined as a generally used medium of exchange. Bitcoin does not meet that definition.

I accept that Bitcoin is a work in progress, and like many others, I await further developments. But I stand by my statement that no private money has been successful if not convertible into a hard asset or assets. Warren Coats’ comment is on point here.

The Fed Was a Mistake. But Now That We Have It…

Gerald O’Driscoll has posted a reply where he raises the question; “Good compared to what?” He cites Larry White’s comparison of monetary stability before and after the creation of the Federal Reserve:

1. The Fed drastically increased inflation compared to the pre-Fed period.

2. The Fed increased price-level uncertainty.

3. The Fed has not reduced real-output uncertainty.

4. The Fed has not reduced the unemployment rate, which calls into question the whole idea of full-employment mandate.

I believe this list is accurate, with the proviso that there is some uncertainty about the pre-1913 period, when data was less comprehensive than today. The next question is what do we make of this failure? Here’s a small list of my own:

1. The creation of the Fed in 1913 was a mistake.

2. It’s not obvious to me that abolishing the Fed and returning to the gold standard is a good idea. (Larry White did not take position on that issue.)

These two statements might seem a bit contradictory, and they call for an explanation. I would argue that Federal Reserve policy errors contributed to the sharp fall in nominal GDP that was the proximate cause of the Great Depression. It should be noted that America’s unit banking regulations also played an important role, by making our banking system much less stable than in countries such as Canada, which allowed branch banking. So why is it not obvious that we should return to the pre-1913 system, if our current system has done worse?

I would argue that two factors point in the other direction. First, the Fed suffered from bad timing, as it was created right on the eve of two devastating world wars. Even if the Fed had not existed it seems likely that there would have been substantial price level instability between 1913 and 1945. On the other hand, without the Federal Reserve there clearly would not have been a “Great Inflation” between 1965 and 1981. So the Fed cannot dodge all responsibility for the increased price level uncertainty.

Fortunately, there does seem to be evidence that long-run price levels are getting more predictable. I’ve been highly critical of Fed policy over the last five years, but even I cannot deny that the current price level is roughly equal to what the Fed promised 10 or 15 years ago, when they first started discussing an inflation target of 2%. That’s actually a pretty surprising result given the severity of the banking crisis and subsequent recession. My point is that institutions can improve over time and the current Fed is almost certainly more competent than the Fed of 1929 – 33 or 1965 – 81. Indeed I believe 20 year-forward price levels are now more predictable than in 1875 or 1895.

I’m very open to proposals that would replace our current discretionary policy regime with a more rules-based approach. That might mean abolishing the Fed; more likely it would involve greatly reducing the Fed’s role in monetary policy, setting a clear monetary standard, and letting markets determine the money supply and interest rates.

In a recent reply, Jerry Jordan raises a very good question:

What should “fed-watchers” be looking at to conclude that enough is enough, it is time to end “pedal to the metal” monetary actions? The Fed is backpedaling off the idea that there is a magic rate of unemployment that will signal the end is near. Scott Sumner suggests nominal GDP will signal when there is too much heat under the kettle. But then what? Nominal GDP jumped from 2.4% in QII to 4.7% in QIII, as the personal consumption price index went from a small decline in the second quarter to 1.9% increase in the third. Suppose NGDP rises further to 6% or higher in the fourth quarter? What should the FOMC instruct the trading desk to do? There is no Federal funds market; the Fed portfolio has no Treasury bills that can be sold.

My point is that there are no rules guiding central bank actions; there is no one inside or outside the Fed who can say anything meaningful about the future.

Mr. Jordan’s comments raise two important issues. First, ideas like nominal GDP targeting (my favorite approach) have less value in a world where the Fed doesn’t have a clear policy objective. If we knew where the trend line was, i.e. what sort of nominal GDP growth (levels and growth rates) that the Fed was aiming at, we could give very clear policy advice. Without such a clear objective it’s hard to know exactly what the Fed should do. I know of NGDP targeting proponents who favor more stimulus than I favor, and others who favor less. And second, the Fed needs a new policy instrument – one that does not become ineffective at the zero interest rate bound. The current policy instrument, fed funds targeting, is like having a car with steering that works most of the time, but locks up when driving on twisty mountain roads with no guard rails. Fed funds targeting seemed to work fine during periods such as the “Great Moderation” of 1985 to 2007, but it doesn’t work at all when we most need it. It’s time to reconsider the Keynesian interest rate-oriented approach to monetary policy.

The Fed Is Creating - and Exporting - Asset Price Inflation

In his essay, Jerry Jordan makes a number of important points. I want to bring attention to one insightful if not provocative statement. “At its root, monetary policy is a fiscal instrument in a fiat currency world.” It is a fiscal instrument because it works by varying the rate of inflation, and inflation is a tax. Viewed that way, monetary policy is a separate system of taxation. That was an argument made cogently by Armen A. Alchian and Reuben A. Kessel in a 1962 scholarly article on the “Effects of Inflation.” Given the recent, loose talk about the benficient effects of higher inflation, their argument is worth keeping in mind.

In a gold or other commodity standard world, central banks cannot generate inflation if they want to stay on the standard. The price level is determined globally by the operation of the commodity standard. It might be better to say there is no monetary policy on a commodity standard. Hence, there is no separate fiscal policy run by central banks.

We have low (not no) price inflation, conventionally measured. But conventional measures are misleading. They exclude asset prices, and by that measure, there are quite strong inflationary pressures. Moreover, these pressures are global. The effects of easy Fed monetary policy work there way both directly and indirectly into the asset prices in other countries. Some countries, like Hong Kong, peg their currencies to the U.S. dollar. The exchange rate of the Hong Kong dollar to the U.S. dollar is maintained within a tight band. The Fed’s creation of U.S. dollars directly impacts the supply of Hong Kong dollars. In practice, that first impacts property values and equity prices in Hong Kong.

As John Taylor and others have argued, even central banks that maintain a floating exchange rate against the U.S. dollar cannot realistically fight Fed policy. To do so would cause a crippling appreciation of the exchange rate of the local currency. Hence, the Fed is exporting global asset-price inflation.

In the meantime, the Fed is engaged in what is called financial repression. By keeping nominal interest rates very low, the Fed ensures that real (inflation-adjusted) interest rates are negative. There is a massive transfer from middle-class savers to favored investors and speculators. The benficiaries are wealthier and bceome more so in the process. They are often politically connected. It is a shocking and largely unremarked regressive income-transfer policy. Once again, it illustrates how monetary policy in a fiat currency world is ficsal policy.

In his further contribution to the discussion, Jordan correctly focuses on Fed governance and the scope for massive discetion. As he observes, there are no rules governing the actions of central banks in a fiat currency world. That greatly exaccerbates the problems discussed above.

Asset Prices, Inflation, and Interest Rates

In his most recent reply, Gerald O’Driscoll has some provocative comments on monetary policy:

In a gold or other commodity standard world, central banks cannot generate inflation if they want to stay on the standard. The price level is determined globally by the operation of the commodity standard. It might be better to say there is no monetary policy on a commodity standard.

It is certainly true that monetary policy is greatly limited under a gold standard. But it’s worth noting that “inflation” is not the only possible monetary policy. The major central banks can and did enact highly contractionary monetary policies during the early 1930s. They did this by sharply raising the ratio of gold to currency, in other words by hoarding massive quantities of gold.

Mr. O’Driscoll is also skeptical of proposals to raise the inflation target, and he makes this observation about price inflation:

We have low (not no) price inflation, conventionally measured. But conventional measures are misleading. They exclude asset prices, and by that measure, there are quite strong inflationary pressures.

Again I partly agree and partly disagree. I certainly agree that inflation is a misleading indicator of the stance of monetary policy. I also agree with Mr. O’Driscoll that it would be a mistake to target a higher rate of inflation. However, I don’t think asset prices are a good indicator either. The real interest rate on 10-year Treasury bonds has been falling for more than three decades, from over 7% to roughly zero. This is clearly not the result of an expansionary monetary policy, as nominal GDP growth (M*V) has also slowed sharply. The lower real interest rates have pushed asset prices much higher for reasons unrelated to monetary policy. Note that low long term real rates are a “fundamental” factor, and hence high assets prices are not necessarily a bubble. In my view nominal GDP growth is the most reliable indicator of the stance of monetary policy, and by that indicator policy has been tighter since mid-2008 than at any other time since Herbert Hoover was president.

Mr. O’Driscoll then points out correctly that monetary stimulus in the United States can result in excessive inflation in countries with currencies pegged to the dollar, such as Hong Kong. But I’m not convinced by this argument:

As John Taylor and others have argued, even central banks that maintain a floating exchange rate against the U.S. dollar cannot realistically fight Fed policy. To do so would cause a crippling appreciation of the exchange rate of the local currency. Hence, the Fed is exporting global asset-price inflation.

If countries with floating exchange rates target nominal GDP growth, then any currency appreciation resulting from the weak dollar will not be “crippling.” In my view the global asset price inflation is coming from a drop in global real interest rates, produced by the same factors that are lowering U.S. real interest rates.

One of the most interesting questions facing monetary policymakers today is the causes and consequences of ultra-low interest rates. I think people like Larry Summers and Paul Krugman are basically correct in their diagnosis of the problem. Structural changes in savings and investment, combined with a 2% inflation target, have made low nominal interest rates the “new normal.” Rates are likely to fall to zero in the next few recessions as well. However I don’t think their solutions are the right way to go. Rather than employing fiscal stimulus, or raising the inflation target, we need to think about a policy of level targeting so that monetary policy remains effective even when interest rates are near zero. Thus I believe we need to find a “third way” between traditional Keynesian arguments and more conservative claims that low nominal interest rates represent an easy money policy.

It is also important to recognize that monetary policy is a “blunt instrument,” not well-suited to popping asset price bubbles. If I’m not mistaken, the only time the Fed ever tried to use monetary policy to pop an asset bubble was in 1929. In that year they continually raised interest rates. At first stock prices continued increasing despite the higher interest rates. Only when interest rates got so high that they drove the economy into a depression did stock prices start falling. In 2011 the European Central Bank tried to move away from very low interest rates by raising their target rate modestly. Unfortunately this drove the eurozone into a double dip recession and they had to cut interest rates back close to zero. Policymakers need to keep their eye on nominal GDP growth.

How Do We Enforce Nominal GDP Targeting?

Scott Sumner has written a thoughtful essay defending targeting nominal GDP (NDGP). As he notes, we agree on some issues and disagree on others. I will respond to a few points.

What I and others have defended was the classical gold standard adopted by the British after the Napoleonic Wars and by America practically in 1879 and officially in 1900. Other major countries adopted that standard at various times throughout the nineteenth century. A number of countries adopted it without having a central bank, e.g., Canada and the United States. To simplify somewhat, it was an automatic system for adjusting the demand for money to the supply of money and maintaining long-run prices nearly constant. (No system is truly automatic if human beings are involved.)

The post-World War I gold standard operated quite differently, and is known in the literature as a gold-exchange standard. Central banks economized on reserves and engaged in the sterilization of reserves that Sumner describes. Both systems (pre- and post-World War I) were called the gold standard, but they were in reality two different systems. Nineteenth century economists like David Ricardo understood the differences very well. Modern economists often conflate them. The global monetary system failed in the 1930s precisely because of the differences between the pre- and post-World War I “gold standards.”

Deficits in the 1960s and 1970s were perhaps modest compared to today, but the emergence of permanent peacetime deficits was a new phenomenon. The story is masterfully chronicled by James Buchanan and Richard Wagner in Democracy in Deficit: The Political Legacy of Lord Keynes. The Fed responded to the new fiscal regime by monetizing the deficits. Fed officials at the time acknowledged what they were doing. It was not a policy error. Politics certainly played a role. Fed Chairman Arthur Burns kept a diary, long secret but now published, of his service in the Nixon Administration. Burns consciously engineered an expansionary monetary policy to help re-elect Richard Nixon. We have it in his own words (Inside the Nixon Administration: The Secret Diary of Arthur Burns, 1969-74, ed. by Robert H. Ferrell). One could describe what Burns did in a variety of ways, not all of them flattering, but there was no policy error here. Nixon wanted “stimulus,” and Burns provided it. The Burns policy greatly contributed to the Great Inflation.

Given this record, I cannot agree that in the 1980s and 1990s “central banks were given greater independence, either tacitly or officially.” There were no official changes, certainly not for the Fed. What changed in many countries was the move away from chronic fiscal deficits. We now know how temporary that change was, and how illusory it was for a number of European countries. In our paper for the 2012 Cato Monetary Conference, “Federal Reserve Independence: Reality or Myth?”, Thomas Cargill and I argue at length against the idea that central banks are independent. The paper appears in the Cato Journal Volume 33 (Fall 2013).

Sumner questions the wisdom of “tamper proof” rules. It is not a phrase that I used, or that I would have chosen. But surely the system of liberalism and constitutional government is predicated on permanent rules. That is what is described in the phrase “the rule of law,” as opposed to the rule of men. I have argued that central banks should be governed by rules for the same reason that government officials generally should be so governed. The rule of law ensures that even evil men can do no great harm. The gold standard is one such rule. Especially as argued in Sumner’s posting for Cato Unbound, NGDP targeting seems too flexible for my taste. Jerry Jordan makes that point in his commentary.

My main question about NDGP targeting, which I have asked Sumner in other forums, is how is the rule going to be enforced? Rules are not generally self-enforcing. If Congress were to mandate some form of NGDP targeting, what incentives do Fed officials have to follow it? Will they lose their jobs if they deviate from the rule? Will their incomes fluctuate with fluctuations in the rate of growth or level of NGDP? (Ben McCallum has recently argued that the difference between rate and level targets is potentially very large.) Central bankers react to incentives, as do all human beings. What are the incentives in Sumner’s system?

The Fed’s Role in Eroding Real Federal Debt

Both Jerry O’Driscoll and Jerry Jordan have emphasized that switching from the rules-based regime of an international commodity standard to a discretionary national fiat standard dramatically loosens the fiscal constraints on the national government. Here are some numbers about how the Federal Reserve has responded to the removal of the gold standard’s constraint against accommodating the U.S. Treasury. The ratio of nominal gross federal debt to nominal GDP stood at 130 percent on the 1st of January 1946, following the Second World War. The monetary base stood at $33.3 billion. Twenty-four years later, on the 1st of January 1970, the debt-to-GDP ratio had fallen to 40%. How was that accomplished?

During the same period the Fed roughly doubled the monetary base (to $62.2b), and as a result the price level (CPI) had roughly doubled. (Real income had grown, of course, but so too had the velocity of the monetary base as a result of the rising inflation that the Fed had created.) The debt ratio fell because the doubling of the CPI contributed to expanding nominal GDP but did not increase the number of dollars owed on previously issued Treasury bonds. The holder of a 30-year Treasury bond issued in 1940-1946 saw more than half of the real value of its principal washed away by inflation. Inflation rates were even higher in the 1970s, such that by 1981 the debt ratio had fallen to its postwar low of 31%. Since then chronic and recently acute deficits have built the debt ratio back up.

In 2012, for the first time since the postwar erosion, the ratio of gross federal to GDP rose above 100 percent. The pressure on the Fed to once again help to erode the real debt is not to be dismissed. Once again the market yields on US Treasury debt do not incorporate any substantial premium for expected inflation. The absence of any rule that prevents unexpectedly inflationary monetary policy means that there is nothing tangible to stop the Fed from once again giving into the pressure to inflate enough in order to reduce the real value of the accumulated federal debt.

Inflation is a Regressive Tax

In a recent post, Larry White usefully reviews a previous occasion that the gross US national debt exceeded the nation’s GDP—the end of World War II. Thanks in part to inflation created by the central bank, in only a quarter century the debt-to-GDP ratio had fallen to only 40%. But while it is important to know this history, it is also important to be careful in the lessons we draw from it.

First, we are not going to see a similar drop in debt-to-GDP in the next quarter century. Why? Because when the war ended, so did the deficits. Larry’s central point is that the debt-to-GDP ratio did not fall to only 40% because the government was running surpluses and paying off the debt. What happened was that a still-large nominal debt became a smaller share of a much bigger GDP, thanks to inflation. However, it was also a period of rapid real economic growth compared to what we are now experiencing.

Today we face far different circumstances: population is growing much more slowly, it is aging rapidly, and the share of adults that are even in the work force has fallen back to the lowest level in over thirty years. Thanks to anti-supply-side taxation and regulatory policies of the national and some of the state governments, a faster pace of real growth will not occur any time soon.

Maybe more worrisome, unlike the end of the war when government stopped deficit spending that was adding to the debt, we now have in place fiscal policies that will be generating large deficits and adding on more debt for years to come. In 1946 we did not face massive unfunded obligations in social security and healthcare programs for seniors, now we do. In 1946 we were at the beginning of several decades of shrinking defense spending as a share of GDP; now we could cut military spending to zero and it would not improve our bleak fiscal outlook.

It also would be an incorrect lesson from history to think that central bank created inflation did not have other adverse consequences. Inflation is a tax that is highly regressive—it worsens the income distribution because low-income people are more likely to rent their homes and have little long-term debt. Inflation transfers wealth from creditors to debtors. Government, as the biggest debtor, certainly gains, but people who have significant real assets such as their homes financed by fixed-rate long-term debt also are on the receiving end of the wealth transfer.

Inflation is a dishonest, divisive, regressive form of taxation—yet politicians prefer to impose it rather than cut spending or raise explicit tax revenue to cover the level of spending. The maxim is, a society that cannot or will not achieve and maintain fiscal discipline will not maintain monetary discipline.

Central Banks Can and Do Hit Inflation Targets

Gerald O’Driscoll has raised a number of interesting issues in a reply to my comments. Here he contrasts the classical gold standard with a gold exchange standard:

The post-World War I gold standard operated quite differently, and is known in the literature as a gold-exchange standard. Central banks economized on reserves and engaged in the sterilization of reserves that Sumner describes. Both systems (pre- and post-World War I) were called the gold standard, but they were in reality two different systems. Nineteenth century economists like David Ricardo understood the differences very well. Modern economists often conflate them. The global monetary system failed in the 1930s precisely because of the differences between the pre- and post-World War I “gold standards.”

I see the situation slightly differently. It is true the gold exchange standard economized on gold reserves, but only up until the late 20s. This is why the interwar price level was higher than the pre-World War I price level. The real problem was that key central banks began to move back towards the classical gold standard in the early 1930s. By 1933 prices had fallen back close to the prewar level, as central banks replaced currency reserves with gold. The problem wasn’t so much the gold exchange standard or the classical gold standard, but rather that transitioning from a gold exchange standard toward a classical gold standard is extremely deflationary.

Mr. O’Driscoll also argues that the Great Inflation was a result of deliberately expansionary monetary policies, not policy mistakes. But why not both? Let’s suppose that during the 1960s policymakers had a “naïve” view of the Phillips curve. They assumed that the trade-off between inflation and unemployment was permanent. They assumed that the Fed could buy lower unemployment with a bit more inflation. We now know that this is wrong, but it appears to have been widely believed at the time. This mistaken view of the Phillips curve led policymakers to adopt an expansionary monetary policy, assuming that they could generate low unemployment with perhaps 3% inflation. They were wrong, and instead we ended up with 13% inflation by 1980. Had they known in 1965 that this sort of monetary policy would lead to 13% inflation, policy might well have been less expansionary in the late 1960s. Yes, Mr. Burns appears to have been corrupt, but surely not all 12 FOMC members were corrupt?

Mr. Driscoll argues that a sounder fiscal policy allowed the Fed to bring down the rate of inflation:

Given this record, I cannot agree that in the 1980s and 1990s “central banks were given greater independence, either tacitly or officially.” There were no official changes, certainly not for the Fed. What changed in many countries was the move away from chronic fiscal deficits.

And yet in the United States fiscal policy became substantially more expansionary during the 1980s as deficits increased under a policy of tax cuts and higher military spending. At the same time, the inflation rate fell sharply, a result that contributed in no small part to the replacement of old Keynesianism with new Keynesianism. Of course we’ve seen the same pattern since 2008, vastly larger deficits and lower inflation.

We also disagree on nominal GDP targeting:

My main question about NDGP targeting, which I have asked Sumner in other forums, is how is the rule going to be enforced? Rules are not generally self-enforcing. If Congress were to mandate some form of NGDP targeting, what incentives do Fed officials have to follow it?

I have advocated the creation of nominal GDP futures markets, which would allow the market to set the money supply and interest rates at a level expected to lead to on target nominal GDP growth. A purely automatic system. However, I strongly believe that nominal GDP targeting, level targeting, could work reasonably well under our under current monetary policy set up. Not perfectly, but reasonably well.

In recent decades the Fed has aimed for roughly 2% inflation, and the policy outcome has been far from optimal. But it’s important to note that the reason for this suboptimal policy outcome is not a failure to keep inflation close to 2%. In fact the rate of inflation in the United States and Canada has been relatively close to 2% for several decades. So I have no reason to doubt that the central bank is able to adhere to a nominal target. The real problem is that 2% inflation is not consistent with macroeconomic stability, whereas stable growth in nominal GDP would be consistent with macroeconomic stability.

I don’t believe that Congress has the expertise required to set a specific macroeconomic target, but rather should set a broad outline, such as the “dual mandate” for stable prices and high employment. Then it’s up to economists in academia and at the Federal Reserve to translate these broad goals into a coherent policy rule. There is a general consensus that monetary policy cannot raise employment in the long run. Thus the Fed has quite reasonably interpreted “high employment” as an unemployment rate close to the natural rate. And stable prices have been interpreted as a low but positive rate of inflation for various reasons. Because it’s very difficult to estimate the natural rate of unemployment, I believe that nominal GDP targeting is a more effective way of addressing the broad goals Congress laid out in the dual mandate (as compared to alternatives such as the Taylor Rule).